Free business advice to help grow your NZ trade business. We will help you identify the Xero apps to suite your individual business needs. Here's how you can take advantage of this limited-time offer.

Recent changes to trust legislations have added another layer of complexity to the management of your assets. Here's how settlors and beneficiaries are captured in the new rules.

Gen Z now make up 24% of the workforce – but is your business culture attuned to the needs of this new generation? Find out how to evolve your company and attract Gen Z talent.

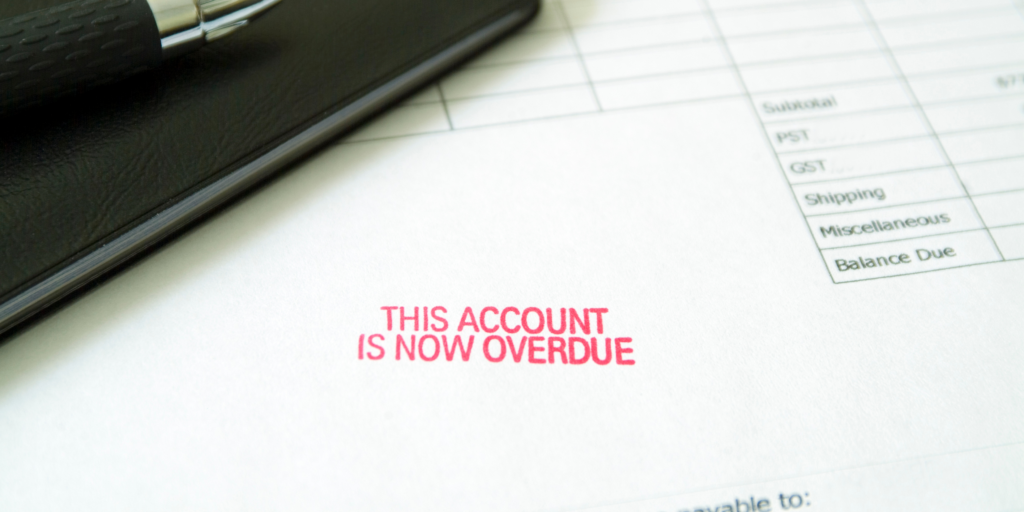

As a small business owner, trying to chase payments while not annoying your clients can be a challenge. Here are 5 tips for getting those outstanding invoices paid while maintaining good relationships.

Do you know the best way to manage a project budget? We can help you build solid, workable, and trackable budgets. Read to understand the benefits of managing cashflow and budgeting on your projects.

It’s end of financial year – time to start thinking about your annual accounts. What do you need to pull together so we can get it right and help your business succeed? Read to find out more.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok